The largest re-pricing event in fine jewellery in fifty years.

India's lab-grown diamond jewellery market is ~₹8,000 Cr today — and on track to cross ₹25,000 Cr by 2030 at current growth rates.

Lab-grown diamonds are chemically, optically and physically identical to mined stones — same IGI grading, same 4Cs, same fire — at 10–30% of the price.

Between 2022 and 2026, lab-grown has moved from 0.4% to ~8% of Indian diamond retail. It is on the same curve the US market walked — where LGD now represents over 50% of engagement ring sales.

India Category Share

8%

LGD retail, 2026 (from 0.4% in 2022)

US Benchmark

50%+

LGD share of US engagement rings

India LGD Market

~₹8,000 Cr

2026 · on track to ₹25,000 Cr by 2030

Price Delta

70–90%

LGD vs mined, like-for-like

02 / 42

Category Momentum

India is where the US was in 2018.

The category's S-curve bends sharply between 5% and 30% share. That is the window in which brand leadership is decided.

US · 2018

~4%

LGD share, engagement rings

US · 2022

~28%

4-year vertical move

US · 2024

~50%

LGD overtakes mined

India · 2026

~8%

Inflection point now

The Indian consumer is two years behind the curve — which means the next three years will do in India what 2018–2022 did in the US. That is when the category's first ten crore-scale brands will be built.

03 / 42

Capital Has Noticed

Indian D2C jewellery re-rated 3–8× in 24 months.

Between Q1 2024 and Q1 2026, every credible LGD or D2C-jewellery brand cleared a step-up round. One IPO, one strategic exit at ₹17,000 Cr. Figures below are post-money valuations, not amounts raised.

Brand

What They Did

Earlier Round · Raised / Valuation

Latest Round · Raised / Valuation

Re-Rating

Palmonas

Pune-based demi-fine D2C (LGD + 18k vermeil + silver). Shraddha Kapoor co-founder. Profitable at ₹39 Cr FY25 revenue with ₹4.3 Cr PAT — rare in D2C jewellery.

₹55 Crraised

₹550 Crpost-money

Series A · Aug 2025

→

₹373 Crraised

₹1,950 Crpost-money

Series B · Mar 2026

3.5×

Aukera

Bengaluru luxury LGD house. Founder Lisa Mukhedkar (ex-PGI) pulled Peak XV in 10 months. ARR ~₹200 Cr by Dec 2025 from 13 stores.

₹26.7 Crraised

₹124 Crpost-money

Series A · Aug 2024

→

₹128 Crraised

₹604 Crpost-money

Series B · Jun 2025

4.5×

Limelight

India's largest LGD brand by stores. 85+ EBOs by FY26. Bhathwari + Emerald Group backed. Shilpa Shetty added as equity-investor + ambassador.

~₹8 Crraised ($1M)

₹340 Crpost-money

Strategic · Apr 2024

→

₹250 Crraised ($27M)

~₹650 Cr+post-money

Series A-II · Dec 2025

~2×

Jewelbox

Kolkata sibling-led LGD D2C. ~₹30 Cr lifetime equity (V3 Ventures, JIIF). Post-money undisclosed across both rounds — shown here on ARR growth instead.

₹3.8 CrFY23 ARR

→

₹40 CrFY25 ARR

~10× ARR

Giva

D2C silver+gold+LGD. ₹523 Cr FY25 revenue (+89% YoY). 240+ stores. Anchor: Premji Invest re-upping every round since 2023.

₹255 Crraised

~₹2,140 Crpost-money

Series B-ext · Oct 2024

→

~₹630 Crraised (C + ext)

₹4,900 Crpost-money

Series C-ext · 2025

2.3×

Bluestone

D2C → omnichannel → IPO. Listed Aug 2025 at ₹8,200 Cr on ₹1,770 Cr FY25 revenue (4.6× P/S). The first VC-built D2C jewellery IPO in India.

₹550 Crraised

₹3,360 Crpost-money

Series F · Sep 2023

→

₹1,540 Crissue size

₹8,200 Crmarket cap

IPO · Aug 2025

2.4×

CaratLane

2008-founded. Tata bought 62% in 2016 at ₹575 Cr, then bought out remaining founder stake in Aug 2023 for ₹4,621 Cr cash at ₹17,000 Cr — 7.8× revenue, 30× the 2016 price.

Palmonas — ₹1 Cr revenue to ₹1,950 Cr valuation in 24 months.

Pune-based demi-fine D2C (LGD + 18k vermeil + silver). Pallavi Mohadikar + Amol Patwari founded 2022; Shraddha Kapoor joined as co-founder Mar 2024. The strongest "this category compounds" comp in the Indian record.

Xponentia Capital (₹179 Cr lead) + Vertex Growth Fund + Vertex Ventures

₹373 Cr

₹1,950 Cr

Cumulative Raised

~₹435 Cr

$50M across 4 rounds

FY25 Revenue

₹39 Cr

40× YoY · ₹4.3 Cr PAT (profitable)

Stores

~70

100-store plan announced post-Series A

Valuation Step-Up

3.5×

Series A → Series B in 7 months

What this proves for Blu Diamonds

A Pune-based D2C jewellery brand went from ₹1 Cr revenue to a ₹1,950 Cr valuation in 24 months — and turned profitable. Indian Tier-1/2 consumers will pay D2C jewellery brands a real multiple when the unit economics work. Palmonas is mixed-material; Blu Diamonds is the pure-LGD luxury wedge.

Aukera — Peak XV underwrote luxury LGD at ₹604 Cr.

Bengaluru luxury LGD house. Lisa Mukhedkar (ex-Platinum Guild International, India category lead) and Kumar Saurabh founded Oct 2023. Cleared a 4.5× re-rating in ten months — the closest single proxy for what we're trying to do.

India's most respected institutional VC underwrote a luxury-positioned LGD jewellery brand at ₹604 Cr post on ~13 stores and ~₹35 Cr revenue. The category is being valued on retail-luxury multiples, not e-commerce ones. Blu Diamonds is the same playbook, one round earlier.

Limelight — India's largest LGD brand. 85+ stores. 7 rounds.

Mumbai-based, founded 2019 by Pooja Sheth Madhavan. Structurally backed by Bhathwari Group (claimed world's largest LGD producer) and Emerald Group (Asia's largest jewellery manufacturer) — vertical integration + Shilpa Shetty as ambassador-investor.

Date

Round

Lead / Investors

Amount

Post-Money

May 2023

Seed

Bhathwari + Emerald Group (parent backers)

n/d

n/d

Apr 2024

Strategic

Industry strategic investors

$1M

₹340 Cr

Feb 2025

Series A

Fund houses, broking firms, family offices, promoters

A vertically-integrated LGD brand can sustain 60–230% YoY growth and attract institutional capital every 12–18 months. Limelight's capital-heavy retail+manufacturing strategy is exactly the kind of overhead a leaner D2C-first premium brand can undercut on margin. We compete on aesthetic, not capacity.

Kolkata-based sibling-led D2C+retail. Nipun Kochar (CEO) and Vidita Kochar Jain founded May 2022. 8 stores by Apr 2025. Design-velocity model — 300 new designs/month, exclusive India rights to the 80-facet "Padma Cut." This is the conservative-comp anchor for Blu Diamonds' raise.

Date

Round

Lead / Investors

Amount

Post-Money

Mar 2024

Seed

JITO Incubation Foundation (lead, ₹2.97 Cr) + family/friends

A capital-light path also exists. Jewelbox cleared ₹40 Cr ARR on ~₹30 Cr lifetime equity, with no Series A yet — proof the category supports capital-efficient scaling. Blu Diamonds' raise is at a comparable stage with a stronger flagship anchor and a deeper unit-economics base.

Bengaluru D2C jewellery (silver → gold → LGD) founded Apr 2019 by IIT Kanpur engineer Ishendra Agarwal. The benchmark for what's possible if Indian D2C jewellery is run with discipline. Premji Invest re-upped in every round since 2023 — five times over.

Indian D2C jewellery compounds to ₹4,900 Cr+ in under 6 years on a silver-led base — without LGD as the hero. Early backers have already returned ₹166 Cr cash to LPs. A pure-LGD brand with higher AOV economics, the same omnichannel playbook, and an institutional path can credibly underwrite a multi-thousand-crore terminal outcome.

Founded 2011 by Gaurav Singh Kushwaha. 14 years from seed to mainboard listing on Aug 19, 2025 — at ₹8,200 Cr market cap on ₹1,770 Cr FY25 revenue (4.6× P/S). Backed at various points by Accel, Kalaari, Saama, Ratan Tata, IvyCap, Hero Enterprise, Peak XV, Prosus, Nikhil Kamath, Deepinder Goyal.

Public · 2.72× subscribed · price band closed at ₹517

₹1,540 Cr

₹8,200 Cr

Pre-IPO Capital

~$255M

16 rounds across 14 years

FY25 Revenue

₹1,770 Cr

+40% YoY · loss ₹222 Cr

Stores at IPO

275

117 cities · 26 states

IPO Multiple

4.6×

Trailing P/S at listing

What this proves for Blu Diamonds

A clean IPO path exists for Indian D2C jewellery — even while still PAT-negative — when the brand commands category-leader scale. The 4.6× P/S multiple is the public-market anchor for what an exit looks like at ~₹1,500 Cr revenue. Blu Diamonds' FY31 ₹118 Cr base implies a clear bridge to that pathway through Series A and B re-rating.

CaratLane — The ₹17,000 Cr Tata exit. The reference.

Founded 2008 in Chennai by Mithun Sacheti (Jaipur Gems family) and Srinivasa Gopalan. Tiger Global capital in 2011–14, Titan majority buy-in 2016 at ₹575 Cr, and in Aug 2023 Titan bought out Sacheti's remaining 27.18% for ₹4,621 Cr cash at ₹17,000 Cr — the largest D2C jewellery exit in Indian history and the second-largest founder e-commerce exit after the Bansals.

Date

Round

Lead / Investors

Amount

Implied Valuation

2011–14

Series A → D

Tiger Global (across 4 rounds, total ~$58M)

~$58M

n/d

May 2016

Strategic Buy-In

Titan Company (Tata Group) — 62% from Tiger Global

₹357 Cr

₹575 Cr

2016–22

Stake Increase

Titan increased holding to 72.3%

~₹100 Cr

n/d

Aug 2023

Strategic Buyout

Titan buys remaining 27.18% from Mithun Sacheti — all cash

₹4,621 Cr

₹17,000 Cr

Markup · 2016 → 2023

30×

In 7 years · ₹575 Cr → ₹17,000 Cr

FY23 Revenue at Buyout

₹2,169 Cr

+73% YoY · ₹82 Cr PAT (profitable)

Buyout Multiple

7.8×

Revenue · 102× EBITDA (strategic premium)

FY25 Revenue Now

₹3,583 Cr

322 stores · ~9% EBITDA margin

What this proves for Blu Diamonds

Tata Group is an active, repeat acquirer of Indian D2C jewellery — they paid premium multiples at every step (2016, 2019, 2023, 2024) and 7.8× revenue at the founder buyout. The exit pathway is real, recent, and public. Other natural acquirers if Titan passes: Reliance Retail, Aditya Birla, Kalyan, Senco, Malabar — but CaratLane is the precedent that anchors valuation.

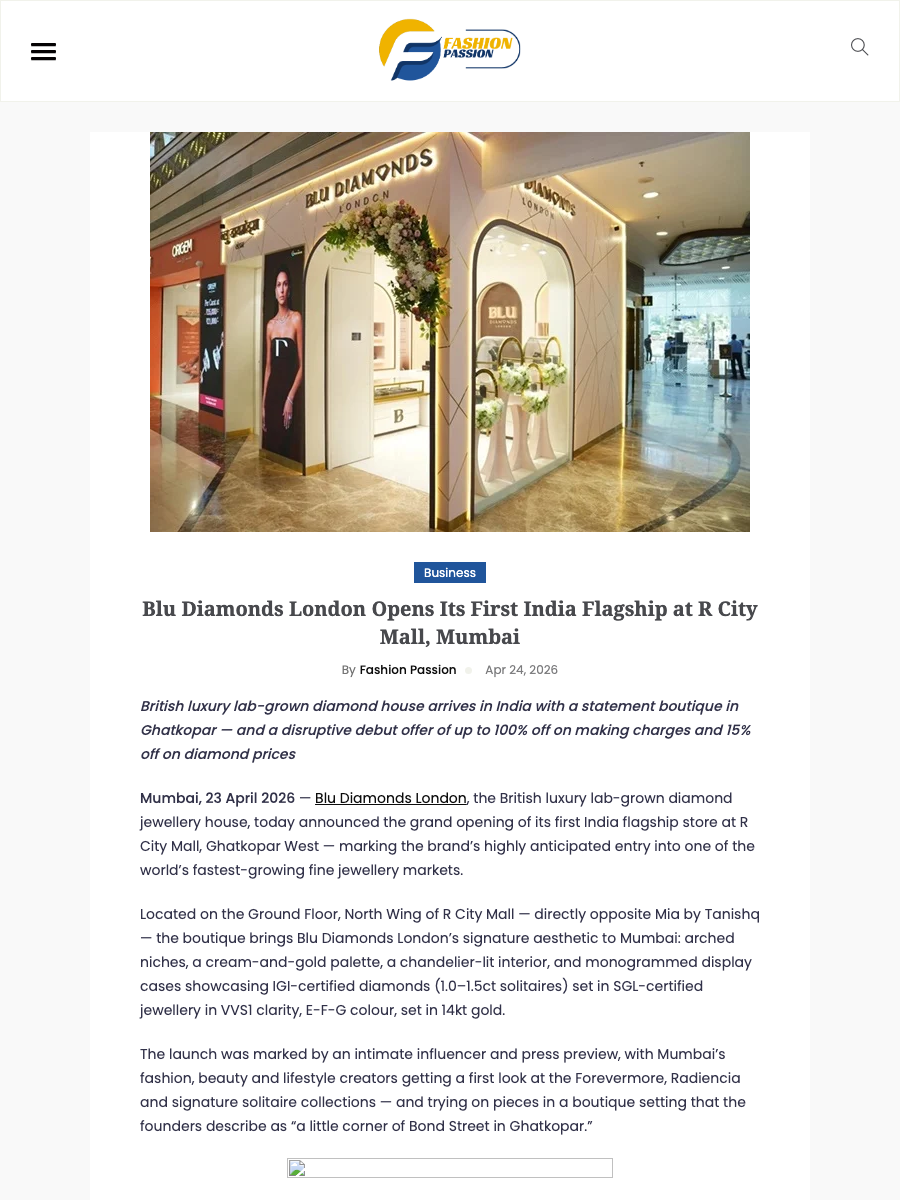

R City Mall, Ghatkopar West — opened with an influencer preview, public in week one. Break-even cleared in the first seven days.

Year 1 Revenue

₹3 Cr

Launch, steady-state + festive — one store

Avg Monthly Run-Rate

₹25 L

1.25× break-even of ₹20 L

Avg Ticket

₹75–80 K

Across solitaires & bridal

Returns / Defects

~0%

Zero quality returns Year 1 — proof of finish

12 / 42

Vision · FY31

India's defining lab-grown jewellery house.

The Indian LGD market is on track to cross ₹25,000 Cr by 2030 — from ~₹8,000 Cr today. The mid-market is already crowded. The luxury position is open. We are building the brand that takes it.

Footprint · FY31

36 stores

COCO-led through FY29 · FOCO / FOFO multiplier from FY29 onward · Mumbai backbone + Tier-2 expansion into under-served affluent markets.

Revenue · FY31

₹118 Cr

21% EBITDA · clean equity cash · no gold-loan leverage · clear bridge to the ₹500 Cr+ scale Bluestone and CaratLane established.

Brand position

Top 3 by rev.

The mid-market is crowded — Aukera, Limelight, Palmonas, Fiona. None have claimed the luxury end of the shelf. That is the position we build for.

Exit pathway

48 mo

Strategic to Titan / Reliance / Aditya Birla, or a Bluestone-style listing. The category has produced one IPO and one ₹4,621 Cr buyout in 24 months.

A British house, built at Indian scale — IGI-certified solitaires, owned inventory, editorial brand voice, omnichannel footprint. The category's first ten crore-scale luxury brands will be built in the next thirty-six months. We intend to be the one that defines the top of the shelf.

13 / 42

Unit Economics

Every store is profitable above ₹20 L / month.

Cost at 1×, priced at 1.8×, sold at 1.6× after launch discount. A blended 37.5% gross margin runs the model.

Single Store — Monthly P&L

Conservative ₹25 L

Steady State ₹30 L

Mature / Festive ₹45 L

Revenue

₹25,00,000

₹30,00,000

₹45,00,000

Cost of Goods

₹15,62,500

₹18,75,000

₹28,12,500

Gross Profit (37.5%)

₹9,37,500

₹11,25,000

₹16,87,500

Salaries · Rent · Marketing · Misc

₹7,50,000

₹7,50,000

₹7,50,000

Store Contribution

₹1,87,500

₹3,75,000

₹9,37,500

Contribution Margin

7.5%

12.5%

20.8%

Store fit-out: ₹50 L premium / ₹30 L tier-2. Inventory of ₹2 Cr per store is carried on the balance sheet as a rotating asset — cash-owned, no debt, no leverage. Payback on fit-out capital: ~18 months.

14 / 42

The Product

Because the right piece is worth planning for.

1.0–1.5ct solitaires, VVS1 clarity, E–F–G colour, 14kt gold. Four signature collections, one discipline: restraint.

Forevermore — bridal. Solitaire engagement rings, matched bands, full sets.

Radiencia — heirloom-coded statement jewellery for wedding functions.

Most brands lead with the stone. We lead with the design.

Bhavin Rupani — co-founder, three decades in fine jewellery manufacturing — leads design and production in-house. Every piece is conceptualised, prototyped, and finished to a single standard. Fancy-colour pink diamonds, baguette settings, marquise architecture, couture-finish tennis pieces — the kind of work the mid-market hasn't built the bench for.

Pink Paradise Bracelet

10.03 ct · Fancy Pink

Pink Whisper Solitaire

3.25 ct · Fancy Intense Pink

Étoile Poire Earrings

8.32 ct · Pear · FG VS

Celée Pendant

Lab-Grown · White Gold

Angelic Drop Earrings

Solitaire · Yellow Gold

Golden Emerald Radiance Ring

Emerald-Cut · 14KT Yellow Gold

Amor Pendant

0.73 ct · Round · 14KT

Seraphic Splendor Bracelet

7.86 ct · Oval + Round

Verdant Glow Trio Earrings

2.85 ct · Princess + Cushion

Ethereal Sparkle Ring

Lab-Grown · 14KT Rose Gold

Eclipse Luxe Pendant

Lab-Grown · Rose Gold

The Valençe Baguette Ring

96 Baguettes · FG VS

Astral Hoop Earrings

Lab-Grown · 14KT

Celesta Solitaire Ring

Solitaire · 14KT White Gold

Marquise Étoile Earrings

6.42 ct · Marquise + Round

16 / 42

The Trust Layer

Two certificates. One at purchase. One forever.

In Indian fine jewellery, certification typically stops at either the stone or the metal. Blu Diamonds is the category's transparency outlier.

IGI — Certified Solitaires

IGI

International Gemological Institute. Every solitaire graded independently on the 4Cs — clarity, colour, cut, carat.

SGL — Certified Jewellery

SGL

Solitaire Gemological Laboratories. Metal purity, stone setting and total weights — independently assayed on the finished piece.

We volunteer both certificates at the billing counter, before the customer has to ask. That single operational choice is our entire marketing positioning.

17 / 42

Launch · Influencer Activation

We opened with 35+ creators. The category noticed.

A hosted dinner at the R City flagship — Mumbai's fashion, beauty and lifestyle creators getting first hands-on with the Forevermore, Radiencia and signature solitaire collections. Every guest left with content. Every piece of content stayed live.

35+ creators · hosted dinner format · reels + collab posts tagging @bludiamondsforever · sustained organic reach across Feb–Mar 2026 — momentum still compounding.

18 / 42

Marketing · Local Distribution

Inside her morning paper. Regularly.

A recurring newspaper-insert programme across Ghatkopar's affluent residential clusters — flyers slipped into Bombay Times, Times of India and Mumbai Mirror. Every household in our catchment opens to a Blu Diamonds A5 flyer carrying the launch offer: 15% off diamond prices · 100% off making charges. Direct-mail economics at print-media trust levels.

A5 flyer · in-house creative · Bombay Times + TOI + Mumbai Mirror · Ghatkopar catchment · recurring drops — the offer enters the home before the customer leaves for work, with the store address, QR and exclusive launch window printed below the fold.

19 / 42

Marketing · In-Mall Visibility

Inside R City. We own the room.

R City pulls one of the highest weekend footfalls in Mumbai retail. We have multiple branded touchpoints across the mall — corridor LED billboards, elevator-bay panels, directional callouts — every shopper sees Blu Diamonds before they reach our door. "Just 50 metres from here. Ground Floor, North Wing." The store doesn't wait for footfall to find it.

Corridor LED billboards · main creative panels · elevator-bay branding — every shopper passes our brand multiple times en route. Launch offer flagged everywhere · 15% off diamond prices · 100% off making charges · store address printed on every panel.

20 / 42

Community · Local Activation

Where the customer already gathers.

We don't wait for footfall — we go where Mumbai's affluent women already congregate. The Jewels Group Mata Ki Chowki gathered 500+ women from the city's upper-middle-class — a curated audience that maps almost exactly to our buyer profile. We were the only fine-jewellery brand on site. Branded standee, dedicated stall, photobooth with QR-driven store callouts.

500+ women · only fine-jewellery brand on site · in-store conversion in the week that followed. Repeatable model — every neighbourhood gathering, kitty club and residential event in Mumbai is a candidate for this playbook.

21 / 42

Marketing · Google Shopping

When she searches, we are already on the shelf.

Google Shopping ads place Blu Diamonds products at the top of every relevant search — "lab grown diamond ring", "solitaire price India", "diamond bracelet online" — with photo, price and brand visible before the user scrolls. Direct-to-product clicks at intent-stage CPCs.

lab grown diamond ring india

ShoppingAllImagesVideosNewsMaps

Sponsored · Shop on Google

Miréva Solitaire Lab Grown Diamond Ring

₹1,46,000

Blu Diamonds London · Free shipping

Ethereal Sparkle Lab Grown Diamond Ring

₹1,72,000

Blu Diamonds London · Free shipping

Golden Emerald Radiance Ring · 14KT

₹2,18,500

Blu Diamonds London · IGI Certified

The Valençe Baguette Lab Grown Diamond Ring

₹1,01,000

Blu Diamonds London · Free shipping

Pink Whisper Solitaire · Fancy Intense Pink

₹2,54,679

Blu Diamonds London · IGI Certified

Shopping feed live across ~600 SKUs · merchant centre + product schema connected · PMax + Search running on bridal, solitaire, gifting and category keywords · catchment-targeted to Mumbai, Pune, Delhi, Bangalore for store-walk and online conversion.

22 / 42

Marketing · Meta Ads

Always on. Every feed, every format.

Reels, Stories, Feed posts, video ads — Blu Diamonds runs across every Meta surface. Branded creative, product-first imagery, store-traffic and WhatsApp-lead objectives in parallel. The feed is where Mumbai's affluent woman discovers what she wants next.

Instagram + Facebook · Reels · Stories · Feed · Video · Carousel · Store-traffic + WhatsApp-lead + conversion objectives running in parallel · WhatsApp-chat CTA built into every ad — the prospect can begin the conversation without leaving the feed.

23 / 42

Digital · India Website & SEO

bludiamonds.com. Built for India.

Full-stack e-commerce on Shopify Plus — ~600 SKUs live, IGI-certificate viewer integrated, EMI plans, WhatsApp-chat enabled, made-to-order flow. Google-review widget on the homepage. Tech SEO foundation locked in: schema markup, product feed to Merchant Centre, mobile-first, fast LCP. The site is the storefront, the salesman and the certificate room.

bludiamonds.com · India · Shopify Plus · owned customer data, no marketplace dependency.

24 / 42

Digital · India Instagram

@bludiamondsforever. 13.2K and compounding.

Organic growth, six months from a standing start. Two festive giveaway moments — Galentine's Day and Akshaya Tritiya — drove the sharpest organic spikes and saved-content volume the account has seen. Branded creative, daily reels and stories, festive campaign mechanics that compound on themselves.

Galentine's Day Giveaway

Feb 2026 · Notable Spike

Akshaya Tritiya Giveaway

May 2026 · Festive Bridal Window

Followers · @bludiamondsforever

13.2K

Reached organically in 6 months — no paid follower campaigns, no follow-for-follow.

Beyond giveaways, a daily reels cadence keeps the feed alive — creator collabs, product hero shots, in-store craftsmanship reels, festive moments. Every reel is shoppable via DM, every collaboration tags @bludiamondsforever, every play deepens the brand's organic footprint.

Creator Collab

@neetanirbhavne × @bludiamondsforever

Product Hero Reel

Emerald + Diamond · Statement Ring

Editorial Reel

Hoops + Stacked Rings

26 / 42

Digital · UK Presence

Blu Diamonds London. UK, live.

The UK arm runs on its own brand surface — blujewellery.co.uk for the storefront, @bludiamondslondon for the editorial. Bridal-led product line, GBP pricing, "Design Your Dream" bespoke flow on the homepage. The London market provides brand provenance; the India market provides scale. Both feed each other.

blujewellery.co.ukUnited Kingdom · E-Commerce

Instagram

@bludiamondslondon

Editorial-led · bridal & engagement focused · British aesthetic carried through every post.

Brand Strategy

London brand provenance — anchors the "British house, built at Indian scale" positioning that the India deck is built on.

27 / 42

Digital · PR Distribution

149 publications. 12M+ network.

The R City flagship launch press release — "Blu Diamonds London Opens Its First India Flagship at R City Mall, Mumbai" — was distributed via India PR Distribution across 149 publications with a combined 12 million+ monthly readership. Built for backlink authority, brand search lift, and a permanent record of category arrival.

Newswire Online

India's Premier Press Release Site

Fashion Passion

Fashion & Lifestyle

Daily Global Reporter

Business News

Startup News Now

Startup & Business

149 publications · 12M+ monthly readership · 24 Apr 2026 · synchronised with R City launch · 149 unique backlinks compounding domain authority and brand search lift. Keywords seeded: Blu Diamonds London · Bridal jewellery · Lab-grown luxury · Sustainable Luxury. Plus 145 more publications across business, fashion, retail and lifestyle.

28 / 42

Brand Face · Insta Live

Ekta Pabari. Our voice on Live.

Actress and brand face. National TV commercial credits include Godrej Secure ("Safety Spells G-O-D-R-E-J" campaign, alongside Omkar Kapoor), TVS and others. She anchors our Insta-LIVE programme — monthly sessions on @bludiamondsforever, walking viewers through new arrivals, festive collections and bespoke pieces, with direct DM-to-store conversion built in. Trusted face, owned channel, live commerce.

Going LIVE in the boutique → Editorial portrait, R City flagship ← New-arrival walk-through · Godrej Secure · TVS · national commercial credits

29 / 42

Marketing · Coming Soon

Mumbai, billboard-scale. Going live.

A city-wide outdoor hoarding programme launching across Mumbai's highest-impact corridors — Western Express Highway, Eastern Express Highway, key Bandra and BKC junctions, premium residential clusters. Editorial brand creative at scale, every hoarding driving directly to the R City flagship. The brand stops being a store and becomes a presence.

BLU DIAMONDSLONDON

Visit the store for exclusive festive offersR City Mall · Ground Floor · North Wing

Outdoor — going live next quarter · creative locked · media slots negotiated · launch synchronised with the festive bridal window. Pre-tested billboard creative shown above — the brand's editorial aesthetic carried into out-of-home at scale.

30 / 42

What We've Already Built

This is not a pitch on a PDF. This is a business that is already running.

Before asking for a rupee, we have built — and are already operating — a flagship, a brand, a digital storefront, a growing community, a certified supply chain, and a financial product.

Flagship Live

R City

Opened with influencer preview. ₹50 L in Month 1. Steady walk-ins, high conversion.

Every diamond + every piece independently certified. Category's transparency outlier.

Leadership

7 strong

CEO, CMO, Design, Gemology, Ops, Tech, Strategy — all in role pre-raise.

Press & PR

Launched

R City launch release issued. Creator content across fashion & lifestyle live this week.

The ₹15 Cr is not to start the business. The ₹15 Cr is to accelerate a business that is already working. Every dependency — brand, product, certification, team, retail operations, financial product, digital channel — is already in place, tested, and generating.

31 / 42

Expansion Engine · FOFO + FOCO

Capital-light scale.

Two ready-to-deploy franchise frameworks unlock the next leg of growth without diluting brand or balance sheet. FOFO (Franchise Owned, Franchise Operated) brings in capital partners who run the store. FOCO (Franchise Owned, Company Operated) brings in capital partners while we keep operational control. Policy documents, financial terms, training programme — all locked.

FOFO Model

Franchise Owned · Franchise Operated

Per-Store Investment

₹3.5 Cr

Inventory + fit-out + working capital + deposit

Term

5 + 5 yrs

Mutual renewal · 30-month lock-in

Franchisee Margin

~30% avg

30% on diamond + 40% on making

Store Footprint

350–1,200 sq ft

High street + mall, brand-adjacent

Franchisor provides: Signage · POS software · creative · staff training · launch support · store manager (on company payroll). Marketing: 50/50 shared.

FOCO Model

Franchise Owned · Company Operated

Capital Source

Franchisee

Inventory + fit-out + working capital

Operations

Blu Diamonds

100% company-run · franchisee passive

Returns to Franchisee

Fixed + Var.

Guaranteed minimum + revenue share

Best Fit

Passive HNI

Real-estate-backed family capital

Why it works: Brand-control fully retained · operations on company SOPs · franchisee gets jewellery-grade returns without operating risk. The model the FY29+ store count is built on.

FY27–FY28: COCO-led (5 stores from this raise). FY29 onward: FOFO + FOCO multiplier — projection model adds 6–11 new stores per year off franchisee balance sheets. Same brand standard, same product DNA, fraction of the equity dilution.

32 / 42

Five-Year Trajectory

₹10 Cr revenue in FY27. ₹118 Cr in FY31. 21% EBITDA.

COCO-led for three years. FOCO / FOFO franchise from FY29 onward — the capital-light growth engine.

Year

FY27

FY28

FY29

FY30

FY31

Store Network (COCO + Franchise)

6

10

16

25

36

Revenue — COCO

₹9.5 Cr

₹22 Cr

₹36 Cr

₹52 Cr

₹70 Cr

Revenue — Franchise

—

₹1.5 Cr

₹7 Cr

₹18 Cr

₹36 Cr

Revenue — Online / Blu Circle

₹0.5 Cr

₹1.5 Cr

₹3 Cr

₹6 Cr

₹12 Cr

Total Revenue

₹10 Cr

₹25 Cr

₹46 Cr

₹76 Cr

₹118 Cr

Gross Profit (37.5% blended)

₹3.75 Cr

₹9.4 Cr

₹17.3 Cr

₹28.5 Cr

₹44.3 Cr

Store Fixed + Central

₹7.2 Cr

₹9.6 Cr

₹12.5 Cr

₹15.8 Cr

₹19.6 Cr

EBITDA

(₹3.45 Cr)

(₹0.20 Cr)

₹4.80 Cr

₹12.70 Cr

₹24.70 Cr

EBITDA Margin

—

~0%

10.4%

16.7%

20.9%

33 / 42

Valuation · Method 1 of 3

DCF says ₹147 Cr. We're asking ₹125 Cr.

Five-year DCF off the operating model, with a conservative 12× FY31 EBITDA exit multiple. Bluestone listed at ~30× implied EBITDA; CaratLane was bought at 102×. We use 12× — well below either. The investor enters at a 15% discount to fair value.

The math, in five lines.

FY31 EBITDA ₹24.7 Cr · exit at 12× = ₹296 Cr terminal enterprise value

Discount to today at 18% WACC over 5 years (1.18⁵ = 2.288) → ₹130 Cr present value of terminal

Across reasonable WACC and exit-multiple assumptions, the DCF brackets ₹105–220 Cr with a base case of ₹147 Cr (18% WACC, 12× exit). We're asking ₹125 Cr — which corresponds to the model's 22% WACC scenario, the most conservative cell in the matrix. The investor enters below DCF base, and the 12× exit multiple is itself ~3× below where Bluestone listed (~30× EBITDA) and ~8× below CaratLane's strategic exit (102×).

34 / 42

Valuation · Method 2 of 3

What does ₹125 Cr return to a seed investor?

FY31 numbers, applied to the comp set's actual exit and listing multiples. The lower entry price compounds — every scenario now clears the seed-stage hurdle by a wider margin.

Strategic CaratLane comp

FY31 revenue ₹118 Cr × 7.8× (Aug 2023 Titan-CaratLane multiple). Tata Group, Reliance Retail, Aditya Birla, Kalyan all active acquirers in the category.

Tactical liquidity at Series A (18–24 months) — Aukera 4.5× in 10 months, Palmonas 3.5× in 7 months. Apply 4× re-rating to ₹125 Cr seed → ~₹500 Cr Series A.

₹500 CrSeries A val

4.0×paper mark

~100% IRRif liquid in 24 mo

The bridge to liquidity. Indian D2C jewellery has produced one IPO (Bluestone, Aug 2025), one ₹4,621 Cr cash exit (Sacheti / CaratLane, Aug 2023), and one ₹166 Cr partial-exit secondary (A91 + IQ at Giva, Oct 2024). The asset class is delivering DPI to early backers, not just paper marks.

35 / 42

Valuation · Method 3 of 3 · Synthesis

Five methods. One range.

Each independent method anchors a valuation range. Plotted on a single 0–300 Cr scale, ₹125 Cr sits at or below the floor of every go-forward method — the investor enters with cushion baked into the price.

DCF · 18% WACC12× FY31 EBITDA exit

₹130 – 185 Cr

Forward Revenue Multiple14–18× × FY27E ₹10 Cr

₹140 – 180 Cr

Series A Precedent · DiscountedAukera Series A ₹124 Cr · Blu @ Seed = 1 round earlier

Replacement Cost · Floor1 live store + ₹2.5 Cr inventory + brand + team of 7 + year of validation

₹15 – 25 Cr

Proposed RoundSeed · ₹15 Cr / 12%

₹125 Cr

₹0₹50₹100₹150₹200₹250₹300 Cr

₹125 Cr is below DCF base (₹147 Cr), below the forward revenue multiple (₹140–180 Cr), below the public-comp discount (₹160–200 Cr). Of the four go-forward methods, only Series A precedent (discounted) places ₹125 in the middle of its range. The replacement-cost floor at ₹15–25 Cr remains the absolute downside. We have deliberately priced beneath the band — early backers buy at a structural discount.

36 / 42

Use of Funds

₹15 Cr, every rupee allocated.

Five new stores in twelve months. Three Mumbai premium locations, two tier-2 launches in under-served affluent markets with zero LGD competitor presence. No debt, no inventory financing — every rupee is equity cash.

Kala Ghoda Flagship South Mumbai · Heritage luxury

₹2.70 Cr

18%

Thane Store Dense affluent catchment · High street

₹2.65 Cr

17.7%

Borivali Store Western suburbs · Bridal market

₹2.65 Cr

17.7%

Nashik Tier-2 · Zero LGD competition · Wedding market

₹2.40 Cr

16%

Nagpur Tier-2 · Affluent Marwari belt · No LGD brand

₹2.40 Cr

16%

Brand · Digital · Influencer Across six stores + online

₹1.20 Cr

8%

Central Team & Tech HQ · ERP · POS

₹0.75 Cr

5%

Working Capital Buffer Festive · Reserve

₹0.25 Cr

1.6%

Total

₹15.00 Cr

100%

Per-store cost: Mumbai ₹50 L fit-out + ₹2 Cr inventory + ₹15–20 L launch = ₹2.65–2.70 Cr · Tier-2 ₹30 L fit-out + ₹2 Cr inventory + ₹10 L launch = ₹2.40 Cr. All inventory owned outright on the balance sheet — no gold loan, no debt, no leverage.

37 / 42

The Ask

₹15 Crore. Twelve percent. One house.

Priced below the Indian LGD comp set — deliberately. We want the people who back us early to win hardest.

Raise

₹15 Cr

All-in round, no debt

Post-Money

₹125 Cr

Below DCF (₹147 Cr) · 12.5× FY27E

Dilution

12%

Clean cap table

Instrument

CCPS / Eq

Investor's preference

38 / 42

The Exit

Series A or strategic within 48 months.

Giva. CaratLane. Bluestone. Indian D2C jewellery is one of the country's most capital-active categories. The precedent is set.

Base · Bluestone Multiple

4.6×

FY31 ₹118 Cr × 4.6× P/S (Bluestone listing, Aug 2025) → ~₹543 Cr exit. ₹125 Cr seed → 4.3× cash · ~34% IRR over 5 years.

Strategic acquirers active in 2024–26: Titan Group (CaratLane buyout, ₹4,621 Cr cash, Aug 2023), Reliance Retail, Aditya Birla Indriya, Kalyan, Senco, Malabar. Institutional path: Peak XV (Aukera Series B), Premji Invest (Giva, 5 rounds), Vertex Ventures (Palmonas), Creaegis, Fireside, Prosus — every one of them has priced an Indian D2C jewellery round in the last 18 months.

39 / 42

Founders & Leadership

Operators, not first-timers.

Bhavin Rupani

CEO

Fourth-generation jeweller. Runs manufacturing, design and supply-chain. Decades of category depth inherited from day one.

Nirav Gosalia

CMO

Operator of businesses at ~600-person scale. Architect of go-to-market, retail aesthetic and digital engine.

Mayank Vora

Head of Strategy

Leads corporate strategy, investor relations, and the franchise & B2B expansion playbook.

Komal Rupani

Head of Design

Rohan Shah

Chief Gemologist

Rahul Goyal

Head of Operations

Harish Patel

Head of Technology

40 / 42

Sources & Methodology

Every number, traceable.

Independent verification across 60+ articles, regulatory filings, and primary cap-table data services. Compiled Apr 2026. Click any source to open in a new tab.

FUNDING DATA — Round amounts and post-money valuations are as publicly disclosed in press releases, lead-investor announcements, or regulatory filings. Where multiple credible figures exist, ranges are used.

REVENUE — From audited filings (Tracxn, Tofler, MCA) where available; otherwise from disclosed press numbers. Indian fiscal year (Apr–Mar).

[ESTIMATE] FLAGS — Used when post-money is derived from disclosed equity / round-amount math (e.g., Fiona Feb 2026 implied post-money from 12% / ₹17.5 Cr).

PUBLIC MARKET DATA — Bluestone IPO per BSE/NSE filings, Chittorgarh, Screener. Titan/CaratLane transactions per Titan Group disclosures + Mint, BusinessToday, Business Standard.

DATA HORIZON — All figures verified between Mar 2024 and Apr 2026. Most recent disclosure used where multiple exist.

41 / 42

The window, and the ask.

The Indian lab-grown diamond category will be won in the next 36 months. We are raising ₹15 Cr for twelve percent, to build the house that wins it.